I filed a Notice of Transfer and Release of Liability (NRL) with the DMV. Why did I receive a notice?

Submitting an NRL to the DMV does not constitute a transfer of ownership. The vehicle record is not permanently transferred out of your name until the DMV receives a completed application for transfer of ownership and payment of appropriate fees from the new owner.

So You’ve had an accident. What Next?

Detailed information on what to do can be found here.

If I was working at the time of the accident is my employer responsible?

California law (https://leginfo.legislature.ca.gov/faces/codes_displaySection.xhtml?lawCode=CIV§ionNum=2338.#:) states that employers are liable for employees’ mistakes .The allocation of responsibility to the employer is also known as “vicarious liability.” Special liability rules apply to Motor Vehicle use under CA vehicle code (https://leginfo.legislature.ca.gov/faces/codes_displaySection.xhtml?lawCode=VEH§ionNum=17150).

What Does It Mean To Be Underinsured?

It means having insurance coverage but the limits may not be high enough (inadequate) to cover the full expense of a claim. Every state has minimum liability coverage for property damage and bodily injury in order to permit/register a vehicle on the road. These minimums, however, are typically not sufficient enough to cover the costs of repair or medical injury. In such cases you may have to pay out of pocket to cover the difference between the limits of coverage and the actual claim.

Even worse if the other party decides to sue the limits will be used for defense costs instead of repayment making you possibly liable for more. While underinsurance may result in lower premiums the loss arising from a claim may far exceed any marginal savings.

Do I have to report an accident to DMV (SR-1 Form)?

California law (as well as most states) requires traffic accidents on a California street/highway or private property to be reported to the Department of Motor Vehicles (DMV) within 10 days if there was an injury, death or property damage in excess of $1,000. The law requires the driver to file this SR 1 form (https://www.dmv.ca.gov/portal/uploads/2020/05/sr1.pdf) with DMV regardless of fault.

Failure to submit the DMV form can result in a suspension of your driver’s license for one year.

There are additional requirements for accident reporting (https://leginfo.legislature.ca.gov/faces/codes_displayText.xhtml?division=10.&chapter=1.&lawCode=VEH)

Do I need to report an Accident to My Insurance Company?

In short, yes; regardless of fault because all Insurance Policies contain a provision called “Duty To Cooperate”.

This provision is based on two concepts: preventing collusion between the insured and the party who created the accident/loss and the second reason is to assist the Insurance Carrier in its investigation, defense of and settlement of a claim or suit. It also enables the Insurance Carrier to obtain relevant information regarding the loss while the information is fresh, to enable it to decide its obligations and to protect itself (and possibly the insured) from fraudulent and false claims. The cooperation clause requires honest cooperation and telling the truth. The duty to cooperate generally extends to providing information to the investigation of the claim, providing testimonial evidence, otherwise cooperating in the defense of the claim and acting in a way so as to not compromise the resolution of the claim. Because this cooperation can be fairly characterized as a “duty” the failure to cooperate can result in a coverage denial and possibly the carrier entirely dropping the policyholder coverage for breach of contract. The best way to prevent a coverage denial is to do what your Insurance Carrier requires without unnecessary delay.

What is Prop 213 and what does it mean if I am Uninsured?

Prop 213 prevents drivers injured in a car accident from obtaining damages for their pain and suffering even when the accident was not their fault if they lack car insurance or the car they were driving was not covered by insurance.

CIVIL CODE – CIV

DIVISION 4. GENERAL PROVISIONS [3274 – 9566]

PART 1. RELIEF [3274 – 3428]

TITLE 2. COMPENSATORY RELIEF [3281 – 3360]

CHAPTER 2. Measure of Damages [[3300.] – 3360]

ARTICLE 2. Damages for Wrongs [3333 – 3343.7]

3333.4. (a) Except as provided in subdivision (c), in any action to recover damages arising out of the operation or use of a motor vehicle, a person shall not recover non-economic losses to compensate for pain, suffering, inconvenience, physical impairment, disfigurement, and other nonpecuniary damages if any of the following applies:

(1) The injured person was at the time of the accident operating the vehicle in violation of Section 23152 or 23153 of the Vehicle Code, and was convicted of that offense.

(2) The injured person was the owner of a vehicle involved in the accident and the vehicle was not insured as required by the financial responsibility laws of this state.

(3) The injured person was the operator of a vehicle involved in the accident and the operator can not establish his or her financial responsibility as required by the financial responsibility laws of this state.

(b) Except as provided in subdivision (c), an insurer shall not be liable, directly or indirectly, under a policy of liability or uninsured motorist insurance to indemnify for non-economic losses of a person injured as described in subdivision (a).

(c) In the event a person described in paragraph (2) of subdivision (a) was injured by a motorist who at the time of the accident was operating his or her vehicle in violation of Section 23152 or 23153 of the Vehicle Code, and was convicted of that offense, the injured person shall not be barred from recovering non-economic losses to compensate for pain, suffering, inconvenience, physical impairment, disfigurement, and other nonpecuniary damages.

(Added November 5, 1996, by initiative Proposition 213, Sec. 3. Applicable, by Sec. 4 of Prop. 213, to actions in which the initial trial has not commenced prior to January 1, 1997. Note: Prop. 213 (The Personal Responsibility Act of 1996) also includes Section 3333.3.)

see also: California Civil Code

What is the Compulsory Financial Responsibility Law

The purpose of the Compulsory Financial Responsibility Law is to ensure that drivers and owners of vehicles are financially responsible for any damage or injury caused by a traffic accident, regardless of fault, and to remove financially irresponsible drivers from the highways.

All the details can be found here.

What area of the country do you work in?

We work throughout the United States. We find that being headquartered in California is beneficial to our success. Our office is open 8 a.m. – 9 p.m. Monday – Friday and 8 a.m. – noon on Saturdays. Due to the time zone differences, we are always available late to contact people at work and at home when trying to determine a settlement.

Can I pay with a debit card?

Absolutely! You can make a one-time Debit card payment or setup a recurring debit card payment via our website.

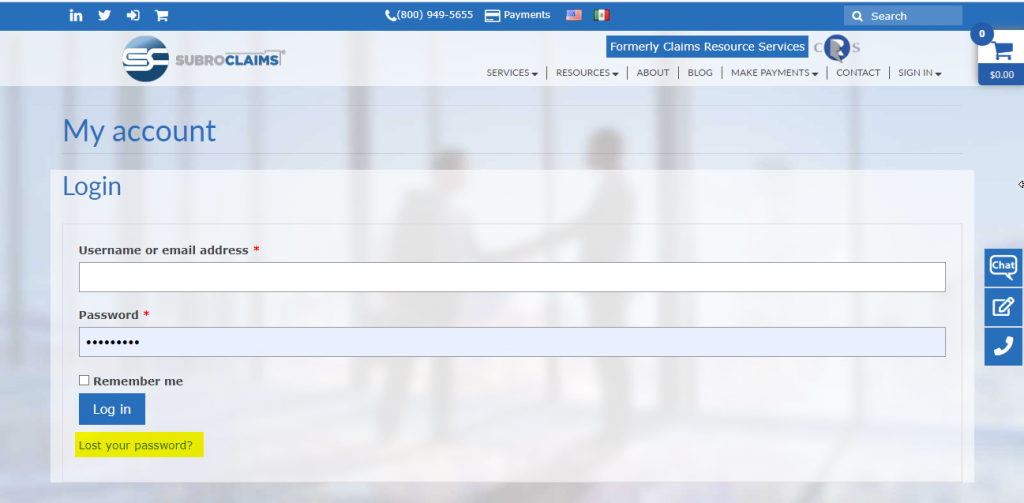

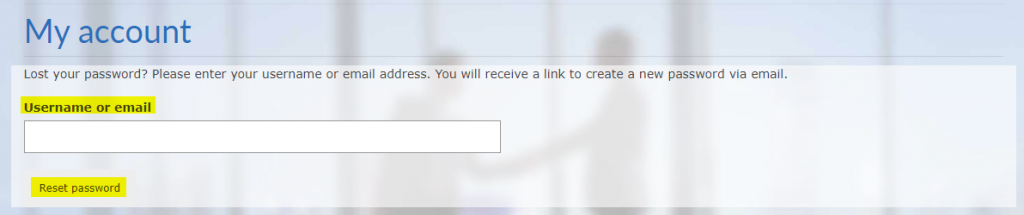

I lost my password – what now?

You can easily reset your password by going to the login page (https://subroclaims.com/my-account/).

- click on “Lost your password?”

- On the next screen, enter your email address and we will send you a link to create a new password.

Do I need an account to make Credit Card Payments?

When you make your first credit card payment (Recurring Credit Card Payment or One-time Credit Card Payment), an account will automatically be created for you. Creating an account for One-time Credit Card Payments is optional but we strongly recommend creating an account as it allows you to track your payments etc.

To login to your account for credit card payments go to MY ACCOUNT (Payments).

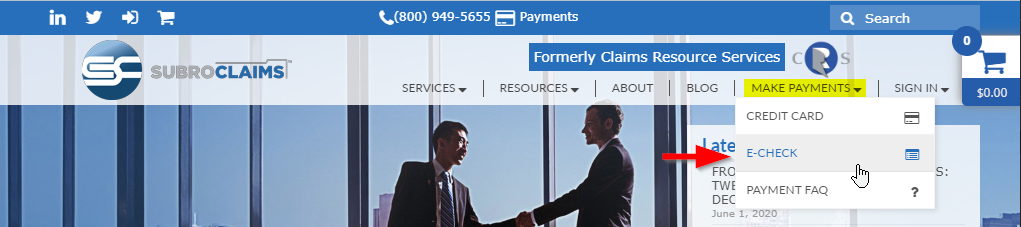

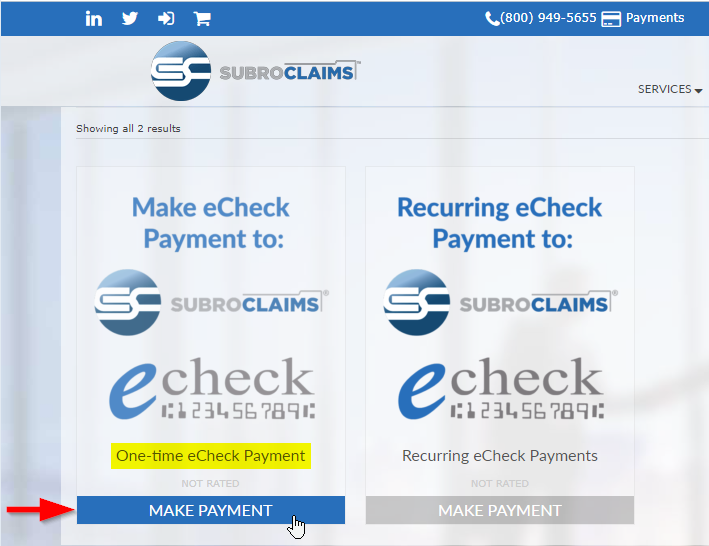

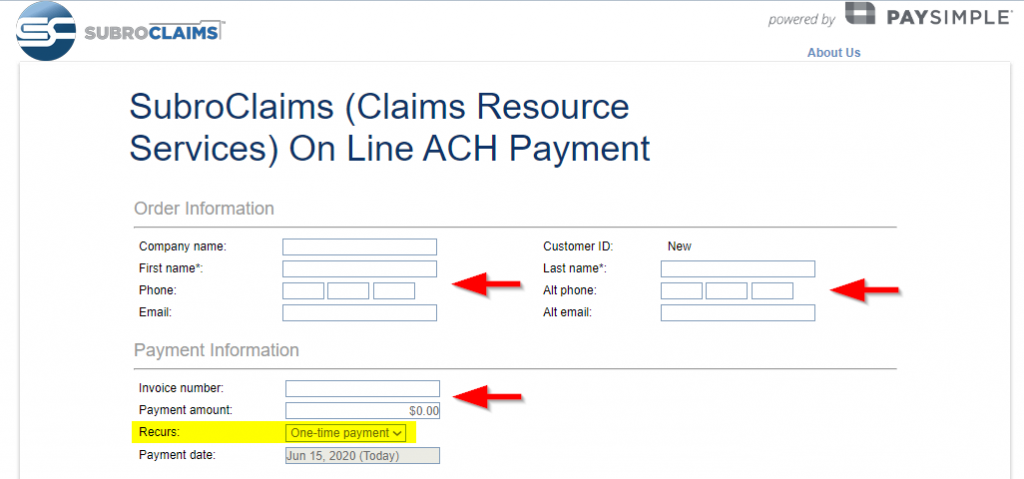

How do I make a single eCheck payment

To make a single eCheck payment, follow the instructions below:

- Select E-CHECK under the MAKE PAYMENTS menu

- Click MAKE PAYMENT under One-time eCheck Payment

- Fill out the E-Check Information. Note: Invoice number = CRSID

- Make sure the “Recurs:” is set to One-time payment

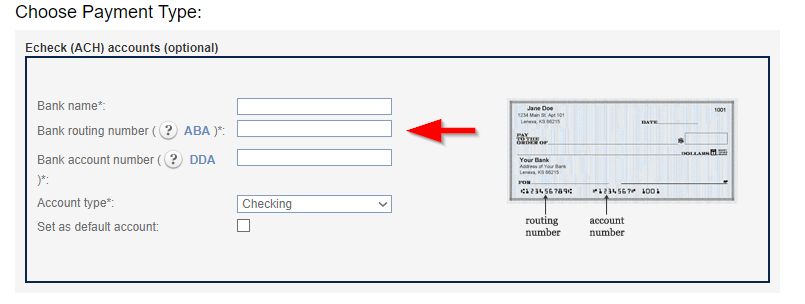

- Enter Checking or Saving Information. Note: For checking the routing number is always 9 digits:

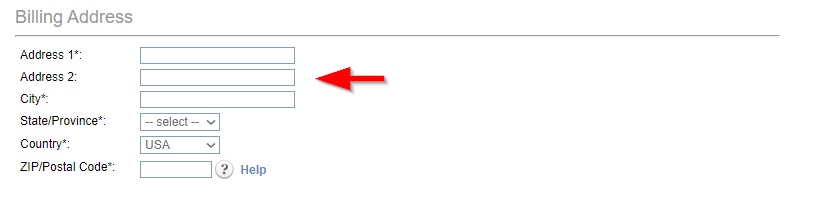

- Enter your billing Information.

Note every box with an * must be filled in

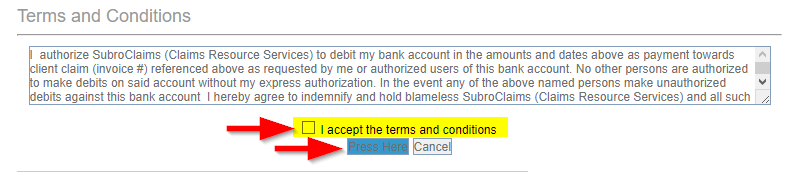

- Enter a User ID and Password to simplify future payments.

- Select checkbox I accept the terms and conditions

- Click “Press Here” to make your payment

- You will receive a transaction receipt via email. Please store for your records.

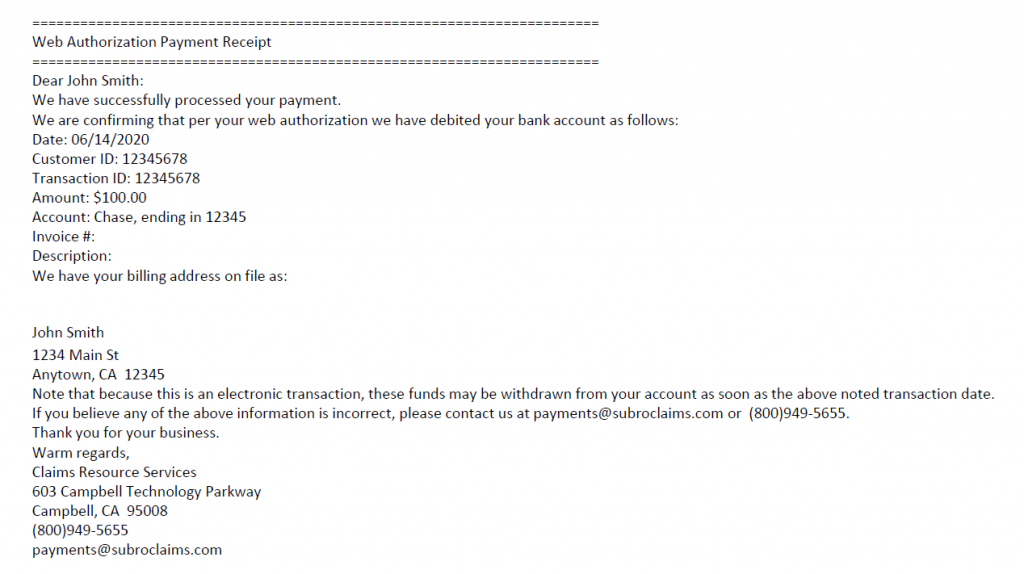

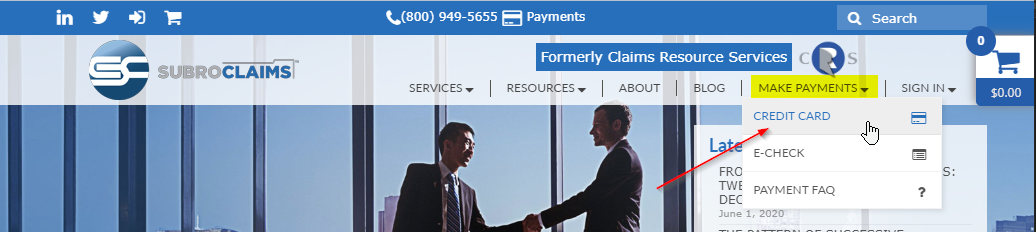

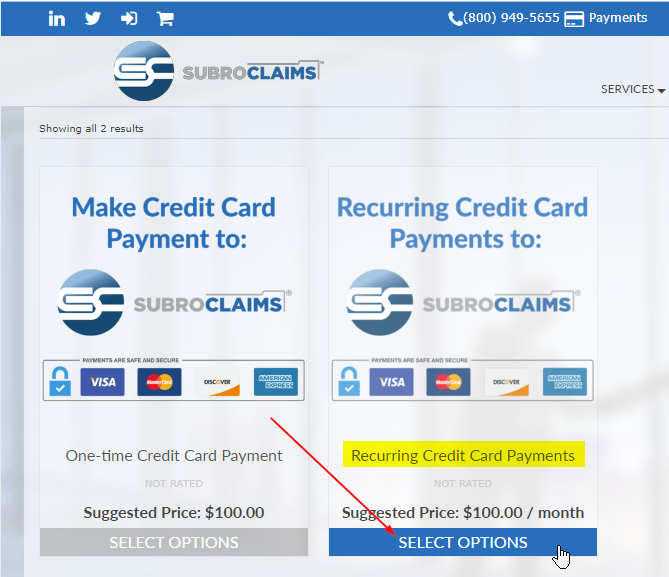

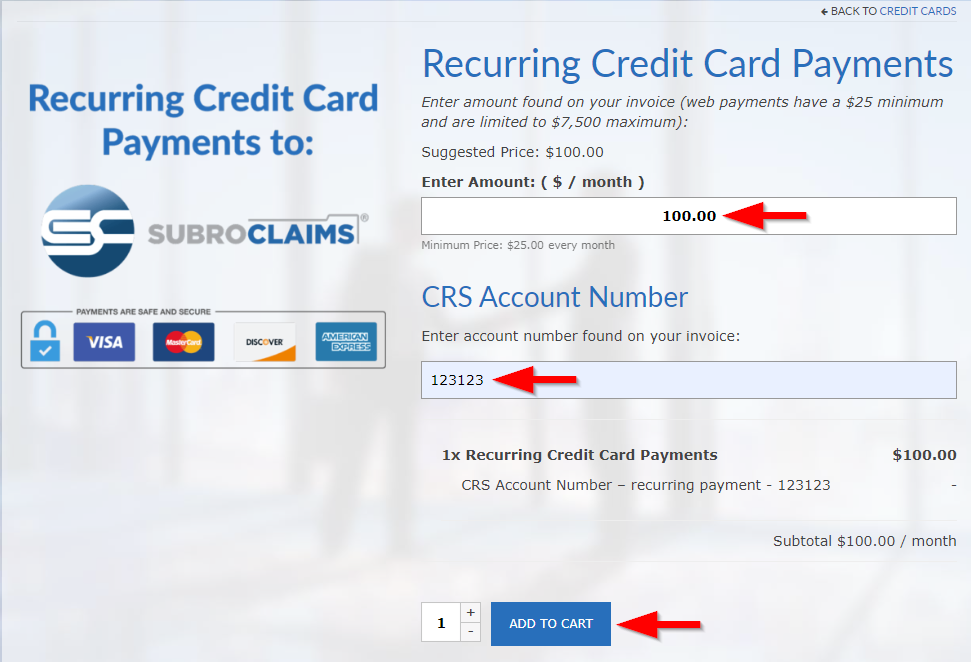

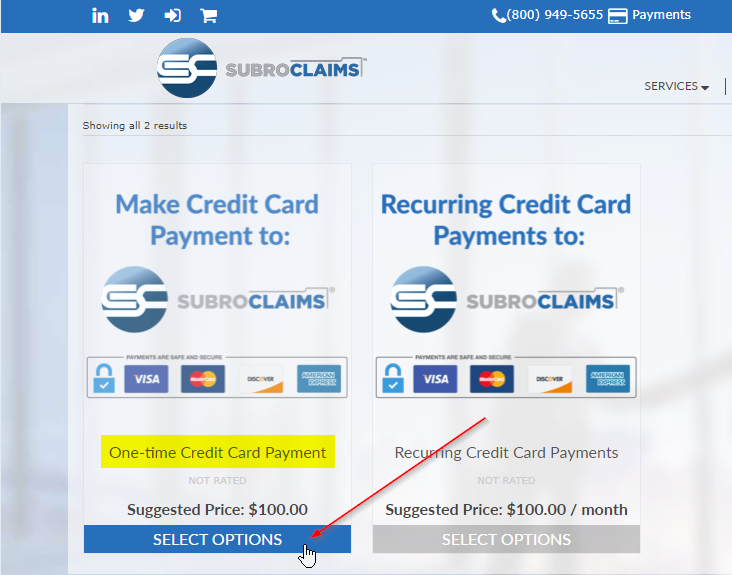

How do I make a recurring credit card payment

To make a recurring credit card payment, follow the instructions below:

- Select CREDIT CARD under the MAKE PAYMENTS menu

- Click SELECT OPTIONS under Recurring Credit Card Payment

- Enter Amount + CRS Account Number + click ADD TO CART

- You will be taken to the shopping cart. When you are ready to make your payment, click Proceed to checkout

- Enter your billing Information.

Note every box with an * must be filled in - Select checkbox I agree

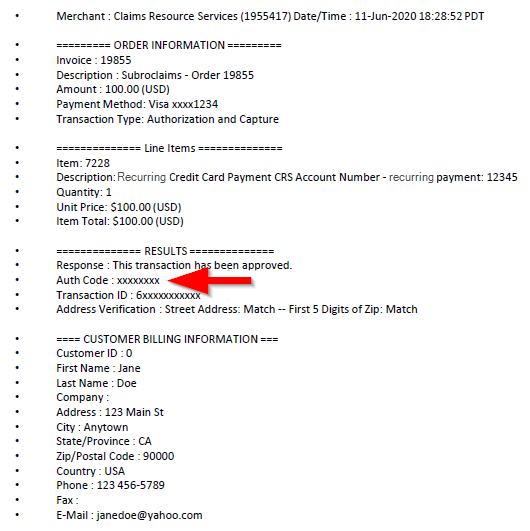

- Fill out the Credit Card Information and click PLACE ORDER

- You will receive a transaction receipt via email. An authorization code is generated on approval. Please store for your records.

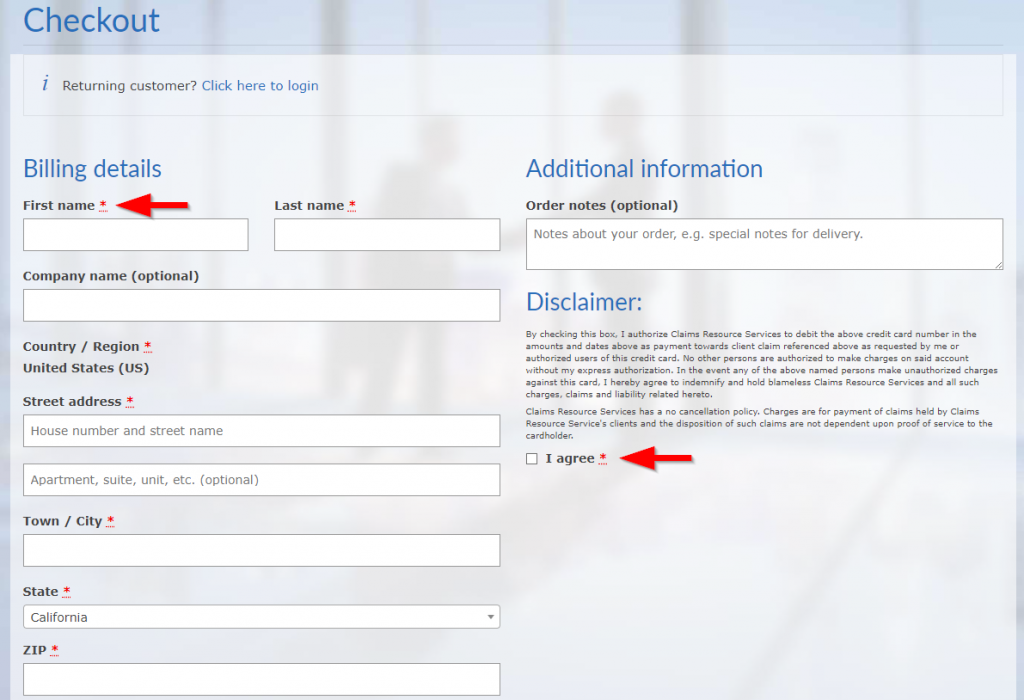

How do I make a single credit card payment

To make a single credit card payment, follow the instructions below:

- Select CREDIT CARD under the MAKE PAYMENTS menu

- Click SELECT OPTIONS under One-time Credit Card Payment

- Enter Amount + CRS Account Number + click ADD TO CART

- You will be taken to the shopping cart. When you are ready to make your payment, click Proceed to checkout

- Enter your billing Information.

Note every box with an * must be filled in - Select checkbox I agree

- Fill out the Credit Card Information and click PLACE ORDER

- You will receive a transaction receipt via email. An authorization code is generated on approval. Please store for your records.

Can I pay with an eCheck

Absolutely! You can make a one-time eCheck payment or setup a recurring eCheck payment via our website.

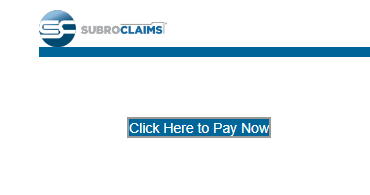

For setting up recurring eCheck payments:

- go to recurring eCheck payment.

- Click on “Click Here to Pay Now” and provide all the required payment info.

- In the “Create Account” section enter your login info and accept terms of service.

- Future payments will automatically be withdrawn from you checking or savings account.

Can I pay with a credit card?

Absolutely! You can make a one-time credit card payment or setup a recurring credit card payment via our website.

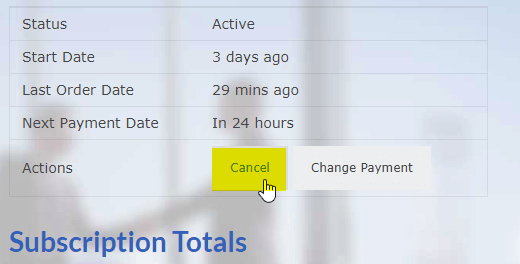

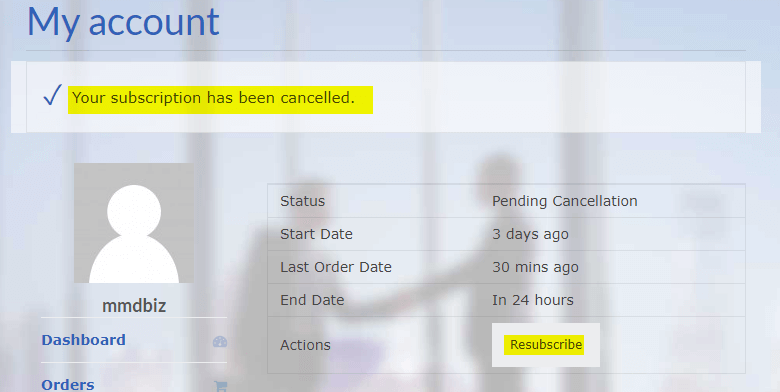

How do I cancel a recurring credit card payment?

You can manage your payments via your account page (login to my-account)

- Click on “Subscriptions”

- Click on “Cancel” to end your recurring payments

- You will see a confirmation message that your recurring subscription has been canceled. You can also easily re-subscribe to recurring payments by clicking the “Resubscribe” button.

I lost my password – what now?

You can easily reset your password by going to the login page (https://subroclaims.com/my-account/).

- click on “Lost your password?”

- On the next screen, enter your email address and we will send you a link to create a new password.

What services do you provide?

We provide all types of subrogation services for our clients who are Property and Casualty carriers and self-insured. We have a collections department, insurance department, arbitration department and litigation department.

What is your pricing?

We develop pricing based on our client and their needs. If you have specific questions regarding our pricing, we would be happy to discuss pricing based on your needs.

What sets Subroclaims apart from other Insurance Vendors?

All we do is subrogation. We have been in business since 1994 providing superior service to our clients through top-notch people, constantly evolving technology and an outstanding management team. With this combination we can recover the most total dollars in the shortest amount of time for our clients.

Who else do you work with?

Subroclaims is privileged to count many National Property and Casualty Insurance Carriers as its clients. We would be happy to provide you a list of references based on the needs you have. Many of our clients take advantage of all of our services, while others only use one or two of our services.

What area of the country do you work in?

We work throughout the United States. We find that being headquartered in California is beneficial to our success. Our office is open 8 a.m. – 9 p.m. Monday – Friday and 8 a.m. – noon on Saturdays. Due to the time zone differences, we are always available late to contact people at work and at home when trying to determine a settlement.

What type of volumes can you handle?

Again, that depends on the type of work you are considering outsourcing and the turnaround time you are expecting. We proactively work with our clients to provide them peace of mind in knowing that the work they send to us will be handled quickly and efficiently without compromising quality. We determine the volume we can handle from our clients based on their needs and our current production schedule.